What is contribution margin?

The result of subtracting all variable expenses from revenues. It

indicates the amount available from sales to cover the fixed expenses

and profit. (Dictionary)

In accounting contribution margin is defined as revenues minus

variable expenses. In other words, the contribution margin reveals how

much of a company's revenues will be contributing (after covering the

variable expenses) to the company's fixed expenses

and net income. The contribution margin can be presented as 1) the

total amount for the company, 2) the amount for each product line, 3)

the amount for a single unit of product, and 4) as a ratio or percentage

of net sales. (Source Q&A)

Source: http://maaw.info/ArticleSummaries/AliExhibit1.gif

Management and accounting web

Lähde : http://users.metropolia.fi/~kuivi/TiVe/Excel/katetuotto.png

{kind=link}

Katso myös tämä http://users.metropolia.fi/~kuivi/TiVe/Excel/excel_3.htm

There is a clear presentation about contribution margin. It is written from Managerial Accounting For Dummies

Contribution margin

measures how sales affects net income or profits. To compute

contribution margin, subtract variable costs of a sale from the amount

of the sale itself:

You can use total contribution margin to create something called a contribution margin income statement. This document is different from a multi-step income statement, where you first subtract cost of goods sold from sales and then subtract selling, general, and administrative costs.

A contribution margin income statement first subtracts the variable

costs and then subtracts fixed costs. Here, variable costs include

variable costs of both manufacturing and selling. Likewise, fixed costs

include more manufacturing and selling costs.

A contribution margin income statement first subtracts the variable

costs and then subtracts fixed costs. Here, variable costs include

variable costs of both manufacturing and selling. Likewise, fixed costs

include more manufacturing and selling costs.

The contribution margin income statement makes understanding cost

behavior and how sales will affect profitability easier. In Figure 9-2,

the company earned $1,000 in sales, $400 of which went toward variable

costs. This scenario resulted in $600 of contribution margin.

The contribution margin income statement makes understanding cost

behavior and how sales will affect profitability easier. In Figure 9-2,

the company earned $1,000 in sales, $400 of which went toward variable

costs. This scenario resulted in $600 of contribution margin.

These amounts — sales, variable costs, and contribution margin — change in proportion to each other. If sales were to increase by 10 percent, then variable costs and contribution margin would also increase by 10 percent; $1,100 in sales would increase variable costs to $440 and contribution margin to $660.

On the other hand, fixed costs always remain the same: The $300 in fixed costs will be $300 regardless of any increase or decrease in sales and contribution margin.

Increasing the sales price doesn’t affect variable costs because the number of units manufactured, not the sales price, is what usually drives variable manufacturing costs.

Therefore, if the gadget company raises its sales price to $105, the variable cost of making the gadget remains at $40, and the contribution per unit increases to $65 per unit ($105 – $40 = $65). The $5 increase in sales price goes straight to the bottom line as net income.

Contribution margin = Sales – Variable costsFor example, if you sell a gadget for $10 and its variable cost is $6, the contribution margin for the sale would be $4 ($10 – $6 = $4). Selling this gadget would increase your profit by $4.

When computing contribution margin, subtract all

variable costs, including variable manufacturing costs and variable

selling, general, and administrative costs. Don’t subtract any fixed

costs. You compute gross profit by subtracting cost of goods sold from

sales. Because cost of goods sold usually includes a mixture of fixed

and variable costs, gross profit doesn’t equal contribution margin.

You can calculate contribution margin in three forms:- In total

- Per unit

- As a ratio

Figure total contribution margin

Total contribution margin measures the amount of contribution margin earned by the company as a whole. You calculate it by using this formula:Total contribution margin = Total sales – Total variable costsTo determine overall profitability, compare total contribution margin to fixed costs. Net income equals the excess of contribution margin over fixed costs.

You can use total contribution margin to create something called a contribution margin income statement. This document is different from a multi-step income statement, where you first subtract cost of goods sold from sales and then subtract selling, general, and administrative costs.

A contribution margin income statement first subtracts the variable

costs and then subtracts fixed costs. Here, variable costs include

variable costs of both manufacturing and selling. Likewise, fixed costs

include more manufacturing and selling costs.

The contribution margin income statement makes understanding cost

behavior and how sales will affect profitability easier. In Figure 9-2,

the company earned $1,000 in sales, $400 of which went toward variable

costs. This scenario resulted in $600 of contribution margin.These amounts — sales, variable costs, and contribution margin — change in proportion to each other. If sales were to increase by 10 percent, then variable costs and contribution margin would also increase by 10 percent; $1,100 in sales would increase variable costs to $440 and contribution margin to $660.

On the other hand, fixed costs always remain the same: The $300 in fixed costs will be $300 regardless of any increase or decrease in sales and contribution margin.

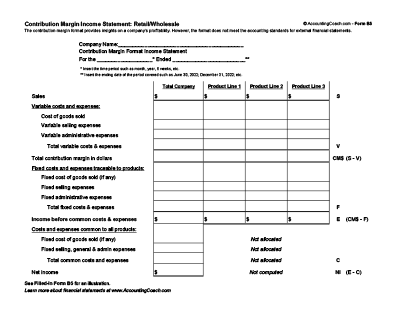

The contribution margin income statement presents the

same net income figure as a traditional income statement. However, the

contribution margin income statement is not in accordance with Generally

Accepted Accounting Principles (GAAP), the set of rules companies must

use for external reporting. Managers can internally use a contribution

margin income statement to better understand their own companies’

operations.

Calculate contribution margin per unit

Contribution margin per unit measures how the sale of one additional unit would affect net income. You calculate it by subtracting variable costs per unit from sales price per unit, as in this formula:Contribution margin per unit = Sales price per unit – Variable costs per unitSay a company sells a single gadget for $100, and the variable cost of making the gadget is $40. Contribution margin per unit on this gadget equals $60 (100 – 40 = 60). Therefore, selling the gadget increases net income by $60.

Increasing the sales price doesn’t affect variable costs because the number of units manufactured, not the sales price, is what usually drives variable manufacturing costs.

Therefore, if the gadget company raises its sales price to $105, the variable cost of making the gadget remains at $40, and the contribution per unit increases to $65 per unit ($105 – $40 = $65). The $5 increase in sales price goes straight to the bottom line as net income.

Work out contribution margin ratio

Contribution margin ratio measures the percentage of sales that would increase net income. To calculate it, divide contribution margin by sales, either in total or per unit:Contribution margin ratio = Total contribution margin / Total sales

or

Contribution margin ratio = Contribution margin per unit / Sales price per unitSuppose a gadget selling for $100 per unit brings in $40 per unit of contribution margin. Its contribution margin ratio is 40 percent:

Contribution margin ratio = 40 / 100 = 40%To find out how sales affect net income, multiply the contribution margin ratio by the amount of sales. In this example, $1,000 in gadget sales increases net income by $400 ($1,000 x 40 percent = $400). (Source: How to compute contribution margin?)

Source: http://www.accountingcoach.com/wp-content/plugins/ac-forms/resources/images/contribution-margin-income-statement-retail.png

{kind=link}

Text Contribution margin Retail/Wholesale

References

Accounting tools

Agronet katelaskuri

Contribution margin (you'll find out a simple calculator)

How to calculate contribution margin? (with pictures)

Kannattavuus ja kannattavuuden osatekijät (tässä blogissa)

Katetuottolaskennasta (tässä blogissa)

Katelaskuja

Kateuottolaskuri

Lähde: http://www.agronet.fi/rypsi2000/images/kevatvehnakate.gif

Viljelyn kannattavuus

Lähde: http://st.merig.eu/fileadmin/user_upload/unit_3/FI/unit3_kapitel_3_2_3_Figure7_fi_.gif

Kannattavuusraja-analyysi

Lähde: http://en.wikipedia.org/wiki/Contribution_margin

Lähde:http://slideplayer.fi/slide/1945045/

Comments